Trump says Iran war "close to over" amid hopes for more negotiations

Introduction & Market Context

First Horizon National Corporation (NYSE:FHN) presented its first-quarter 2026 earnings results on April 15, 2026, demonstrating continued momentum in profitability metrics despite a modest revenue shortfall. The Memphis-based regional bank reported adjusted earnings per share of $0.53, exceeding analyst forecasts of $0.50 by 6%, while revenue of $862 million came in slightly below the $868.91 million consensus estimate.

The company’s stock rose 2.23% in premarket trading to $24.79, reflecting investor confidence in First Horizon’s ability to sustain strong returns through disciplined expense management and effective deposit pricing strategies. With shares up 42% over the past year and trading near the upper end of their 52-week range of $16.45 to $26.56, the bank has demonstrated resilience in a challenging operating environment marked by volatile interest rates and competitive deposit markets.

Quarterly Performance Highlights

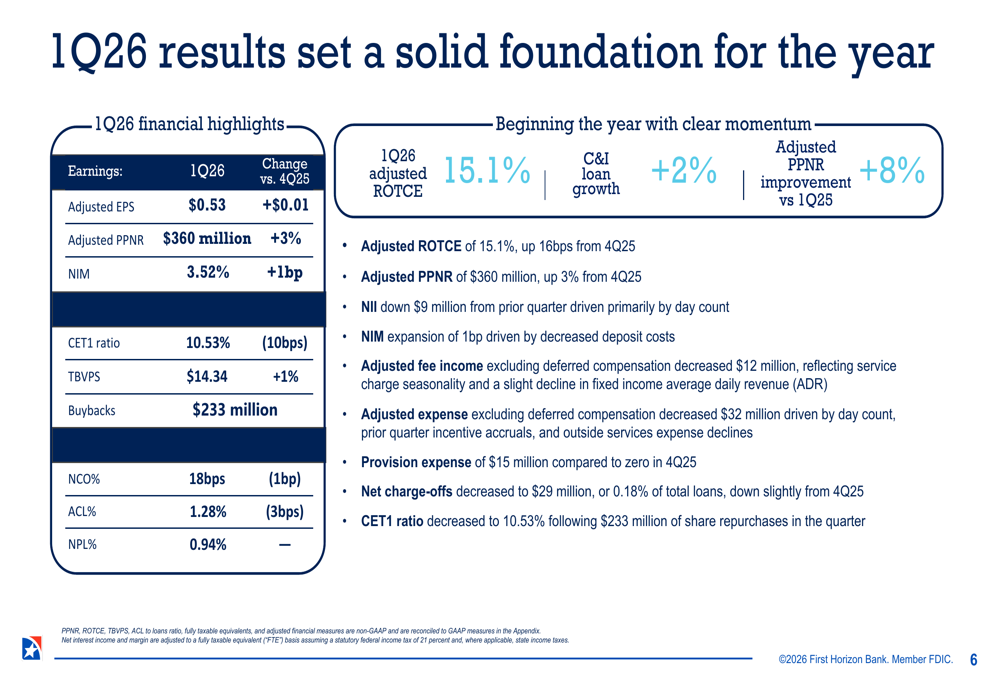

As shown in the following comprehensive financial summary, First Horizon achieved its third consecutive quarter of adjusted return on tangible common equity (ROTCE) above 15%, reaching 15.1% in the first quarter.

The bank’s adjusted ROTCE of 15.1% represented a 204 basis point improvement year-over-year and a 16 basis point increase from the prior quarter, underscoring the sustainability of the company’s profitability trajectory. Adjusted pre-provision net revenue climbed to $360 million, up 8% from the first quarter of 2025 and 3% from the fourth quarter, demonstrating operational leverage despite headwinds from lower day count and seasonal factors.

Net interest income totaled $667 million, up 6% year-over-year but down 1% sequentially, primarily due to fewer days in the quarter. However, the bank’s net interest margin expanded by 1 basis point to 3.52%, driven by continued success in reducing deposit costs. Fee income of $195 million increased 7% year-over-year but declined 8% from the prior quarter, reflecting typical seasonal patterns in service charges and a slight moderation in fixed income trading revenues.

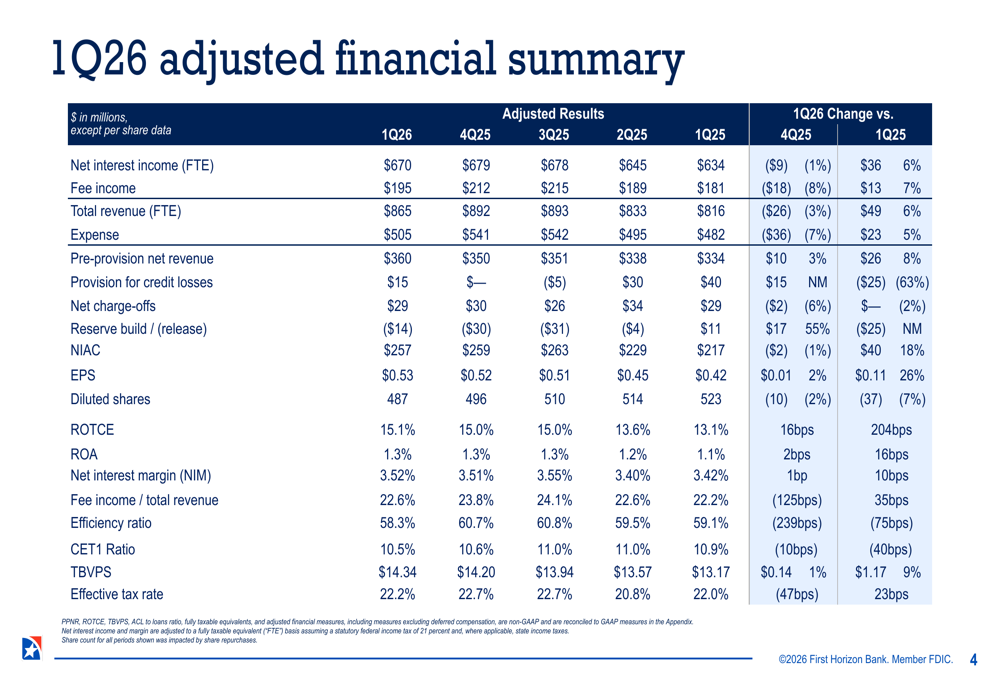

The detailed adjusted financial metrics reveal the strength of the bank’s core operating performance across multiple dimensions.

Detailed Financial Analysis

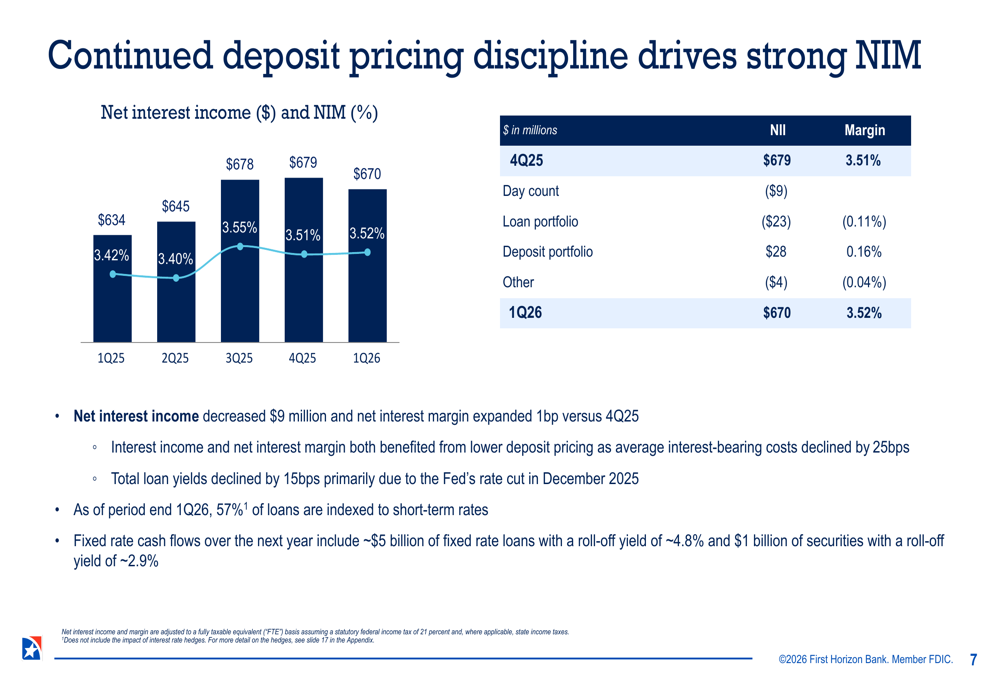

First Horizon’s margin expansion story centers on disciplined deposit pricing in an increasingly competitive environment. The bank demonstrated strong execution in managing its funding costs while retaining customer relationships.

Net interest margin improved to 3.52% despite net interest income declining $9 million sequentially, as the bank successfully lowered its interest-bearing deposit cost by 25 basis points to 2.28%. Management noted that the company retained approximately 97% of roughly $29 billion in total balances associated with repriced deposits during the quarter, highlighting effective relationship banking strategies.

The bank’s asset-sensitive profile positions it well for various interest rate scenarios, with 57% of loans indexed to short-term rates, 12% in adjustable-rate mortgages, and 31% in fixed-rate instruments. Over the next year, approximately $5 billion of fixed-rate loans will reprice from a roll-off yield of 4.8%, while $1 billion of securities will mature at a 2.9% yield.

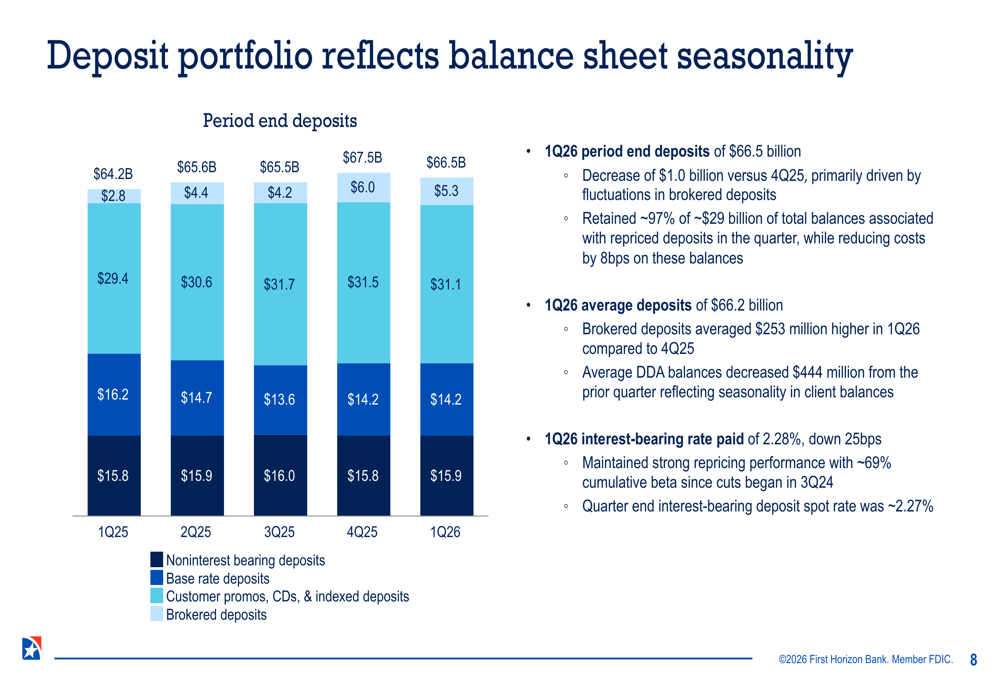

The deposit portfolio reflected typical first-quarter seasonality, as illustrated in the following breakdown.

Period-end deposits of $66.5 billion decreased by $1.0 billion from the fourth quarter, primarily driven by fluctuations in brokered deposits, which the bank actively manages as a funding tool. Average demand deposit account balances declined $444 million from the prior quarter, consistent with seasonal patterns. The bank’s deposit mix shows 24% in noninterest-bearing accounts, with the remainder split between base rate deposits, promotional products, and brokered funding.

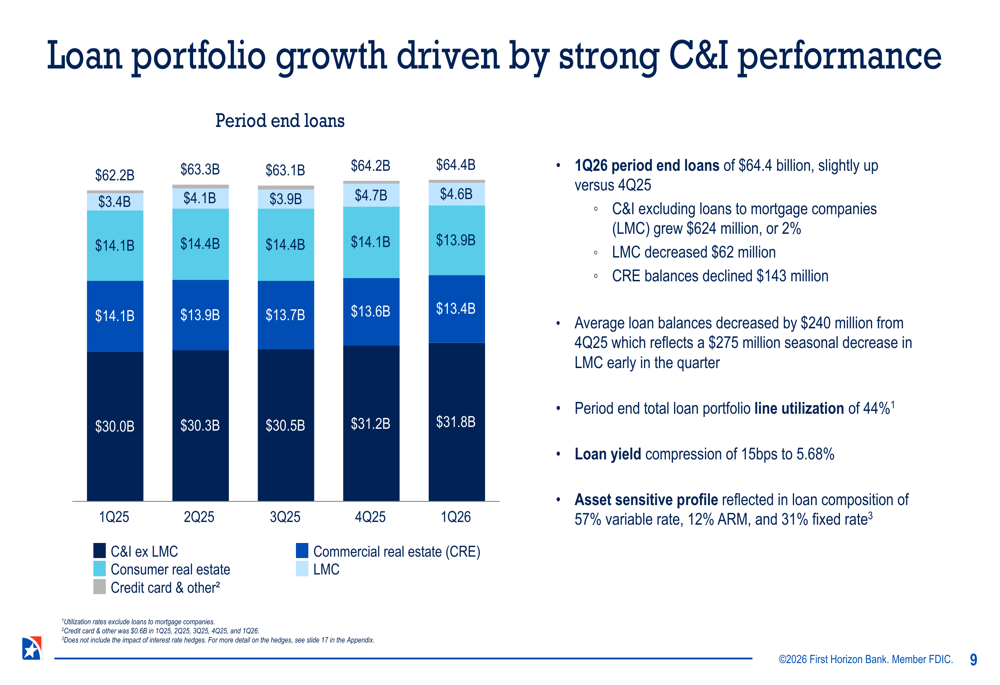

Loan portfolio growth was driven by strong commercial and industrial lending performance, offsetting continued runoff in commercial real estate.

Period-end loans of $64.4 billion increased slightly from the prior quarter, with C&I loans excluding loans to mortgage companies growing to $31.8 billion, up 2% sequentially. This growth came despite a seasonal $275 million decrease in mortgage company lending early in the quarter. Commercial real estate balances continued their managed decline to $13.4 billion, while consumer real estate and other consumer loans totaled $4.6 billion. Total loan portfolio line utilization remained at 44%, suggesting capacity for future growth as economic conditions improve.

Expense discipline remained a key driver of the bank’s improving profitability metrics. Adjusted expenses excluding deferred compensation decreased $32 million from the fourth quarter to $505 million, driven by lower day count, the reversal of fourth-quarter incentive accruals, and reductions in outside services spending. This careful cost management enabled the bank to achieve positive operating leverage despite revenue pressures.

Credit Quality & Capital Management

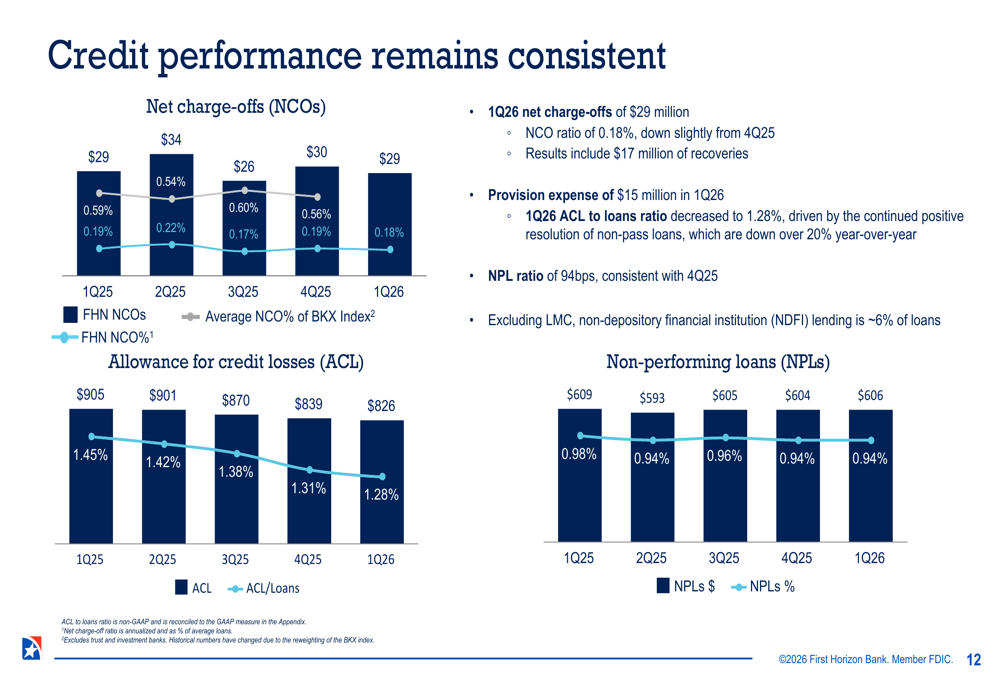

Asset quality metrics remained stable and within management’s expectations, demonstrating the bank’s prudent underwriting standards and effective risk management.

Net charge-offs totaled $29 million, or 0.18% of total loans, down slightly from the prior quarter and well within the bank’s full-year guidance range of 0.15% to 0.25%. The provision for credit losses was $15 million in the first quarter compared to zero in the fourth quarter, reflecting modest loan growth and economic outlook adjustments. The allowance for credit losses to loans ratio decreased to 1.28%, while the nonperforming loan ratio held steady at 94 basis points.

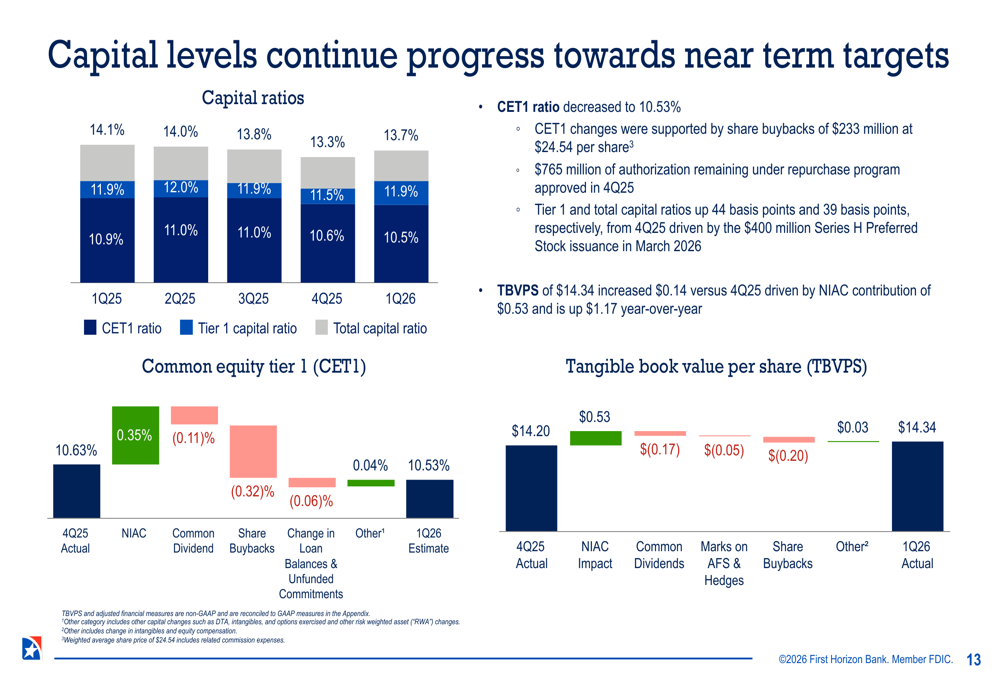

Capital management remained a strategic priority, with the bank actively deploying capital through share repurchases while maintaining regulatory ratios above target levels.

The Common Equity Tier 1 ratio decreased to 10.53% following $233 million of share repurchases during the quarter, remaining comfortably above the bank’s near-term target of approximately 10.5%. Tangible book value per share increased to $14.34, up $0.14 from the prior quarter driven by net income contribution of $0.53 per share, and up $1.17 year-over-year, representing 9% annual growth.

Strategic Initiatives & Outlook

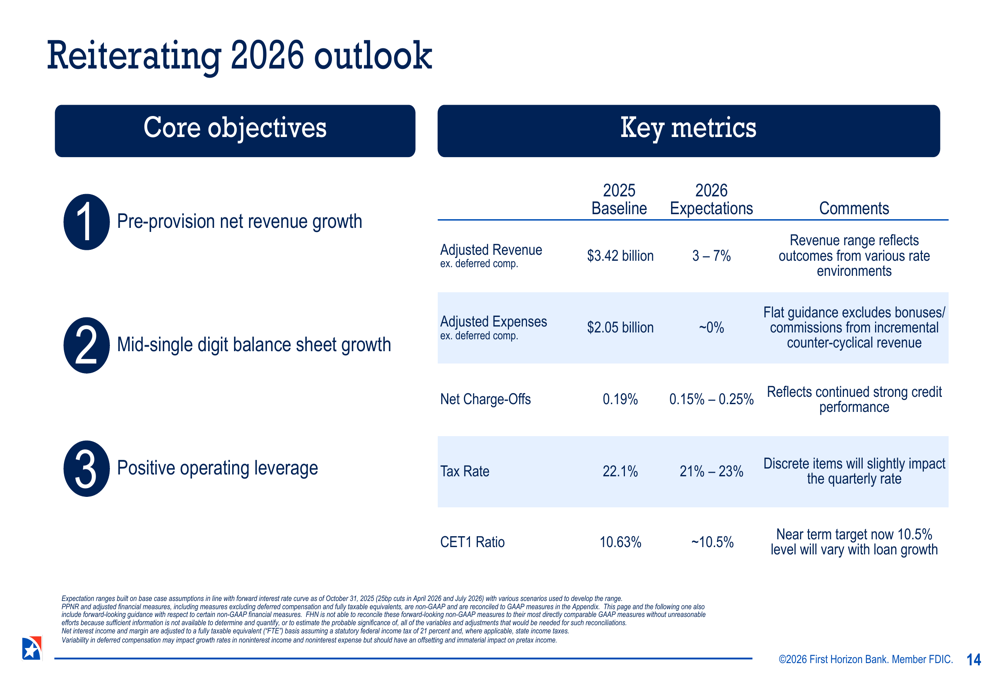

First Horizon reaffirmed its full-year 2026 guidance, projecting continued momentum across key financial metrics.

Management reiterated its outlook for adjusted revenue growth excluding deferred compensation of 3% to 7%, while holding adjusted expenses excluding deferred compensation approximately flat. This guidance implies continued positive operating leverage and pre-provision net revenue growth, with mid-single digit balance sheet expansion expected. The bank maintained its net charge-off guidance of 0.15% to 0.25% and projected a tax rate of 21% to 23%, with the CET1 ratio targeted at approximately 10.5%.

CEO D. Bryan Jordan emphasized the bank’s strategic focus on deepening client relationships and expanding market presence. "Our strong first-quarter results reflect the successful execution of our strategic initiatives and disciplined approach to cost management," Jordan stated during the earnings presentation. "We remain focused on deepening client relationships and expanding our market presence."

The bank outlined key growth drivers including client relationship expansion, maximizing revenue opportunities through product penetration, and continued enhancements to treasury management and wealth management services. These initiatives support management’s confidence in sustaining adjusted ROTCE above 15% through focused execution on client acquisition and retention strategies.

Risk Management & Forward-Looking Considerations

First Horizon’s liquidity and interest rate risk management framework provides a foundation for navigating uncertain macroeconomic conditions.

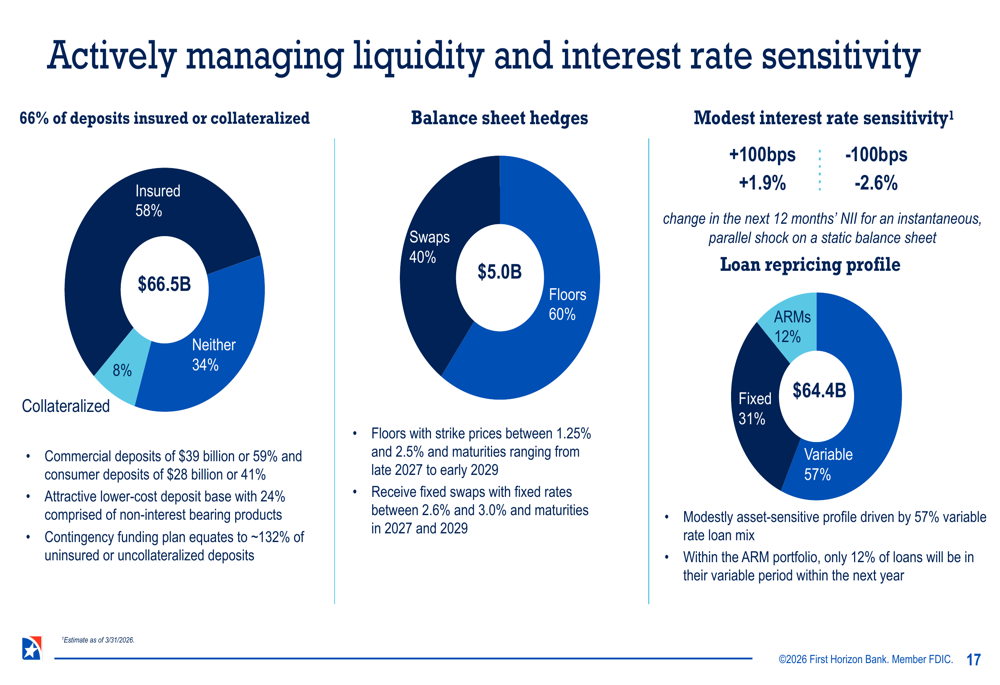

The bank maintains a conservative liquidity profile with 66% of deposits either insured or collateralized, including 58% insured and 8% collateralized. Balance sheet hedges totaling $5.0 billion, split between swaps and floors, provide protection against interest rate volatility. The bank’s modest interest rate sensitivity shows a 1.9% positive impact from a 100 basis point parallel rate increase and a 2.6% negative impact from a 100 basis point decrease.

Management acknowledged several risks and challenges that could impact future performance, including macroeconomic uncertainty stemming from geopolitical factors and volatile interest rates, increased competition in deposit markets that may pressure margins, and potential headwinds in commercial real estate markets that could affect loan growth. The bank’s diversified business model and counter-cyclical revenue streams, particularly through FHN Financial’s fixed income trading operations, provide some offset to these challenges.

With analysts projecting EPS of $0.53 to $0.55 for upcoming quarters and full-year estimates of $2.13 for 2026 and $2.19 for 2027, First Horizon appears positioned to deliver consistent returns while managing through a complex operating environment. The company’s ability to sustain profitability above 15% ROTCE for three consecutive quarters, combined with disciplined capital deployment and expense management, suggests a maturing business model capable of generating attractive returns across economic cycles.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.